Key words

Cost evaluation, laparoscopic cholecystectomy, cost minimization analysis

Introduction

Cholecystectomy is a widely used abdominal operation in the management of symptomatic gallstones, with 15.000 procedures annually in Greece [1] . Gallstones are approximately 10% to 15% of the adult western population and between 1% and 4% become symptomatic every year [2,3] . While conventional open surgery has been the gold standard for over 100 years, small-incision cholecystectomy is a minimally invasive alternative for removal of the gallbladder [4] . Laparoscopic cholecystectomy is the most performed minimally invasive surgical procedure performed by both junior and senior physicians (approximately 15,000–19,000 are performed annually in the Netherlands) [4] . The laparoscopic cholecystectomy has been reported to be a safe and effective method [5-8] . However, the evidence whether this technique results in lower costs for the health care system compared to open operations is not yet conclusive [6–10] . Moreover, in only one randomized controlled study productivity losses were taken into account [11] . Therefore, several economic aspects remain unanswered, mainly due to differences in methods of collecting and reporting costs.

The Greek national health care system [NHS] is financed both through taxation (1/4) and social insurance (1/4) sources, supplemented by a high proportion of voluntary financing (1/2). Hospital care is mainly provided and financed by the state through salary based NHS providers, but also in a significant proportion by social insurance funds (1/3) on a per diem reimbursement [12] . Organizationally, the system is highly centralized and regulated, with virtually every aspect relating to health care financing and provision subject to control by the Ministry of Health [13] .

The aim of this prospective study was to provide further insight in direct and indirect cost of laparoscopic [LC] versus open cholecystectomies [MC] and to define patients’ socio-demographic characteristics that have an impact on economic outcome of laparoscopic technique in a General public hospital in Greece.

Material and Methods

Study design and patients’ characteristics

Sixty seven patients with symptomatic gallstone disease undergoing elective cholecystectomy between September and December 2007 gave written informed consent and were enrolled in the study. During this period, a total of 100 patients were referred to a single surgeon for cholecystectomy in the General Hospital of Chalkida. The General Hospital of Chalkida is the main district hospital of an island next to Athens with a population of over 200.000 people. The hospital has 300 beds and offers health services to the entire population of the district under the auspices of the Greek NHS. Of these, 33 patients (33%) refused to participate. Thus, the study population comprised the 67% of all patients, who were willing to participate. Patients were allocated to open surgery [MC, n=17] or laparoscopic cholecystectomy [LC, n=50] . Since it was a non-randomized study, only patients thought to be surgically suitable candidates for laparoscopic cholecystectomy were selected. Patients having a cholecystectomy as adjunct to other abdominal operations such as pancreatic resection, hepatic resection or operation for aneurysm were excluded from the study.

To obtain data, a structured questionnaire comprising of economic and socio-demographic variables such as gender, age, profession and permanent health insurance plan, was developed and approved initially by the clinical and administrative director. All costs were calculated in Euros. The total [direct and indirect] cost for the services provided for each patient was determined for both interventions. All costs applicable to each of the health services were summations of direct variables, direct [fixed and variables] costs and overhead. We calculated total hospital cost for the pre-, intra- and post-operative ward stay periods. We cost time spent in general surgical ward before and after intervention using the appropriate hospital bed day costs inclusive of hospital overheads, such as hospital administration, building and maintenance costs. Theatre duration in minutes was collected from each patient’s anaesthetic sheets. To cost the use of the theatre per min, finance departments provided a fixed cost per hour for an empty theatre (inclusive of hospital overheads, building charges and routine theatre capital equipment). This cost was applied to the duration in theatre of each of the patients in the sample. Direct costs were obtained for each care area and included, professional fees, drug costs, disposables, medical equipment utilization, diagnostic tests and clinical support services. Direct fixed costs are those related to direct patient care and are relatively fixed regardless of the duration or number of patients. Direct variable costs are the costs related to direct patient care and varied with the duration or number of patients. The medical staff included two surgeons (supervisor and trainee), a nurse and an anesthesiologist. Staffing levels were assumed not to vary between patients. Indirect costs due to loss of productivity were calculated based on an annual average income of 14.000 Euros. The annual income was divided by 230 working days. Under these assumptions, cost per day off work was 61 Euros. We have to mention that we did not assess possible heterogeneity between salaries and wages for indirect cost.

Finally, age was classified in three categories (25-49 years, 50-65 years and more than 65 years), profession in four categories (Farmers-OGA, Traders-OAEE, Employees to Private Sector-IKA in conjuction with Employees to Public Sector- Dimosio and Pensioners) and the corresponding Permanent Health Insurance Fund factor in five categories (OGA, OAEE, IKA, Dimosio and Private Insurance). The study protocol conforms to the principles of the Declaration of Helsinki and was approved by the hospital ethical committee.

Statistical analysis

Descriptive statistics along with Mann- Whitney U, Kolmogorov-Smirnov and Kruskal Wallis H tests were the initial basic statistical tools for data analysis. The distributions of quantitative variables (cost and hospital stay variables) in the two study groups were compared by using the Kolmogorov-Smirnov non parametric test. The Mann-Whitney U test was used to compare the cost between MC and LC methods. Within each method demographical and social economical factors were tested by using the Kruskal Wallis H test. A p-value of less than 0.05 was considered statistically significant. Taking into account cost variables (pre-, intra- and post-operative), a cluster analysis is used to grouping within the dataset. Afterwards, statistical analysis between clusters took place (based either on profession or on insurance plan). Finally, multiple regression analysis was run in order to evaluate the relation among cost and other independent demographic or socioeconomic variables.

Results

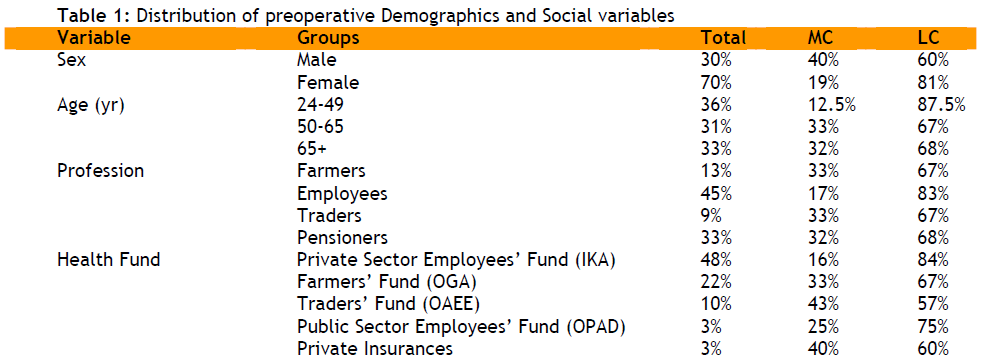

The two groups (MC – LC) were well matched except for the proportion men / women. The proportion male - female is 30% - 70%, the three age groups were equally participated (almost 1/3 each) and the proportion of profession & insurance fund is extremely closed to the national trends [Table 1] .

Cost Analysis

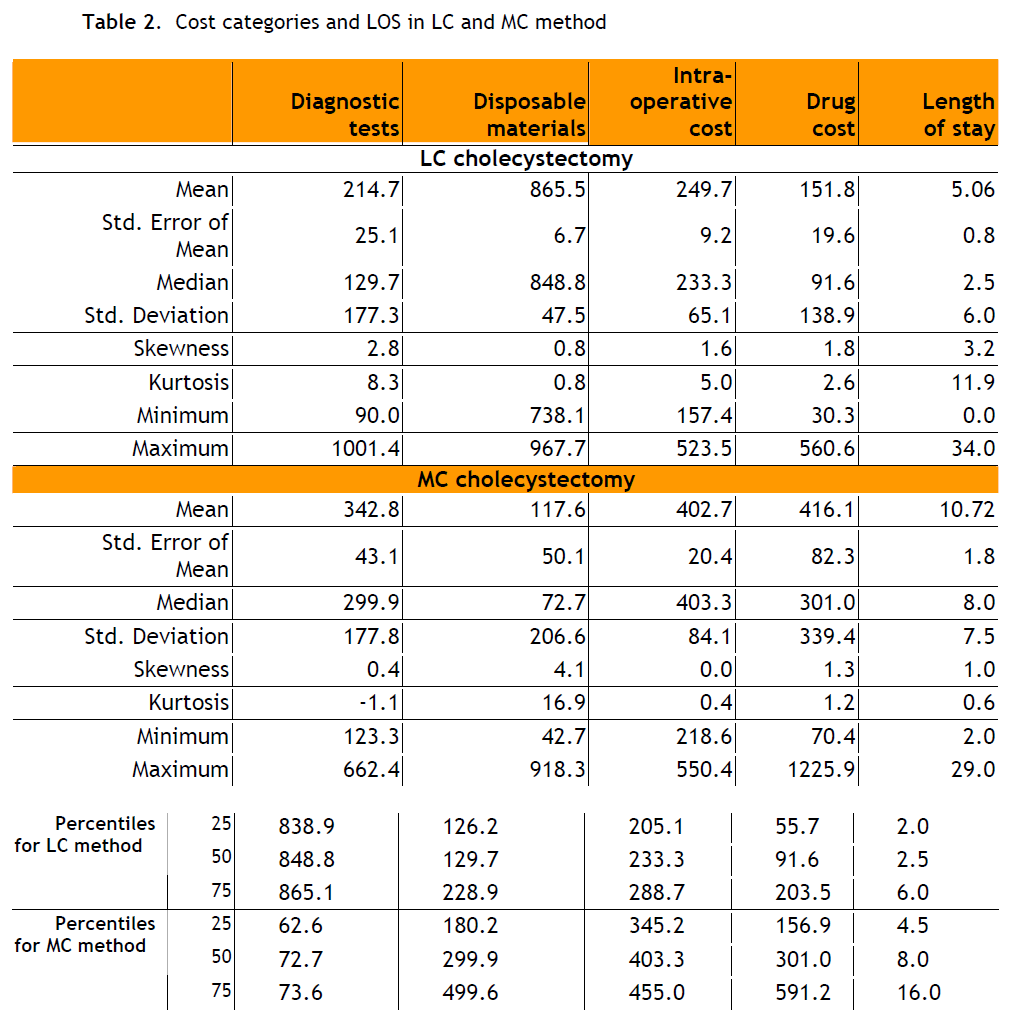

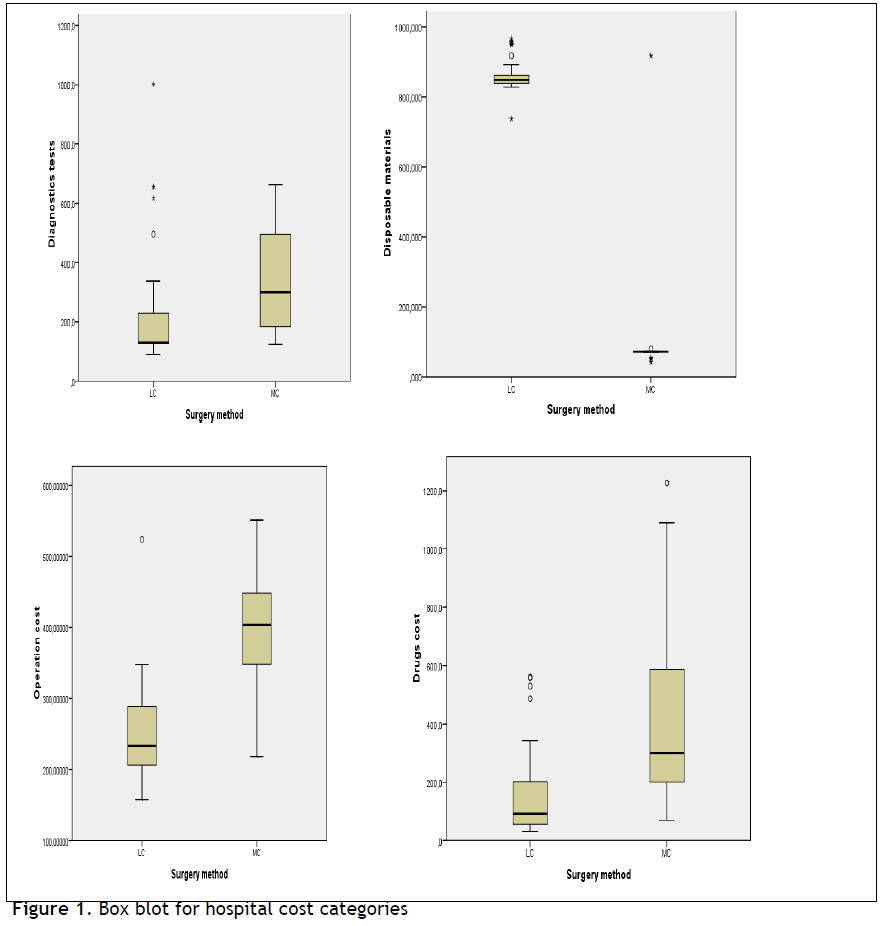

In the cost analysis, the total direct cost was slightly lower in the LC method compare to MC method; an 95% confidence interval for total direct cost in LC group was 1.676±148 Euros versus 1.701±390 Euros in the MC group, p-value =0.645. Further to our cost analysis, hospital cost excluding the “hotel services” cost, shown in Table 2 was quite similar between the two groups [1.482+91 Euros in the LC method versus 1.279± 264 Euros in the MC method, p=0.075] . Analyzing the hospital cost in four categories including disposables, intraoperative, diagnostic tests and drug costs a different distribution was showed between the two methods. For the LC method 58.4% of the hospital cost was consumed for disposables, 14% for diagnostic tests, 16.9% for intra-operative cost and 10.7% for drugs versus 9.2%, 27%, 31.5% and 32.3%, respectively for the MC method, (Table 2 and Figure 1).

Figure 1: Box blot for hospital cost categories

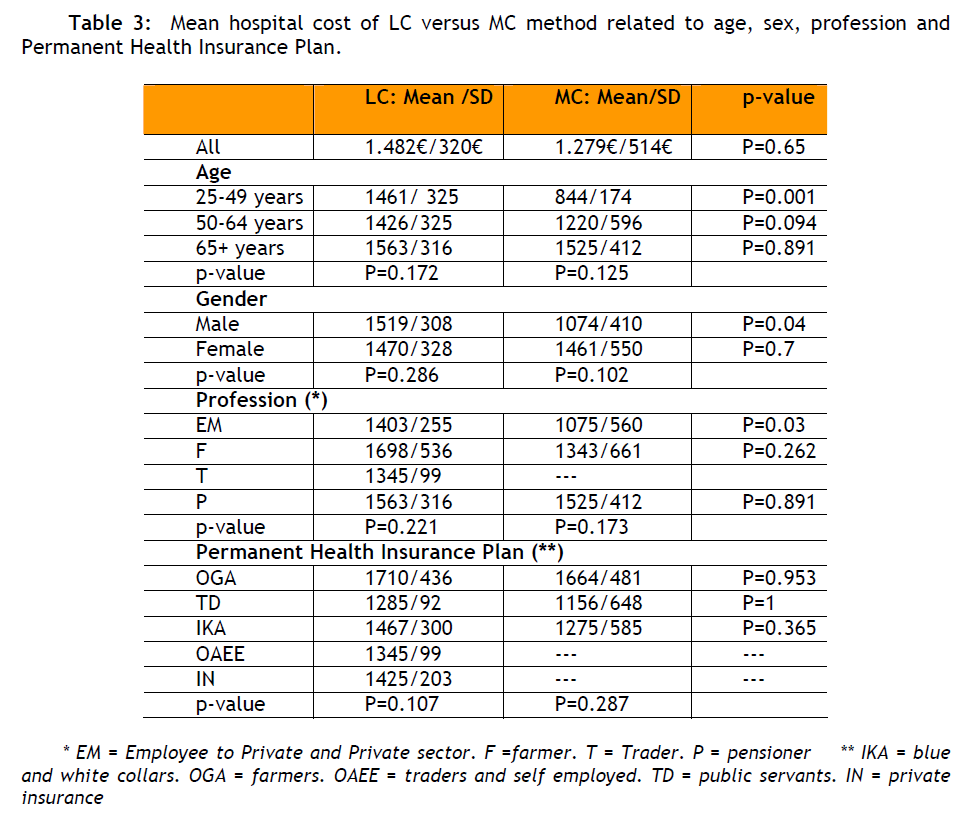

The mean time in theatre was 107 min in the MC group and 75 min in the LC (p<0.001). The mean intra-operative cost was 402.7 Euros in the MC group versus 249.7 Euros in the LC group, p <0.001 (Table 2 and Figure 1). The mean cost was influenced by demographic and social-economic characteristics (Table 3) for male (pvalue= 0.039), age group 24-49 (pvalue= 0.001) and Employers (p-value=0.031).

Analysing the cost of disposable materials, the mean cost was 865.5 Euros for the LC method and 117.6 Euros for the MC method (Table 2), while those costs varied from 738 to 968 Euros for the LC method and 90 to 1.001 Euros for the MC method. Taking into account demographic and social economic factors, within each method, no statistical significant differences were found. The mean cost for diagnostic tests was 215 Euros for the LC method and 343 Euros for the MC method (p<0.05), (Table 2). The average number of tests for the MC method was 8 tests and for the LC method 6.8 tests. Moreover, it must be mentioned that the MC method requires more diagnostic tests post operatively (27% of total tests), compared to the LC method (14% of total tests). For the age group 25-49, the difference between the mean cost for diagnostic tests of each method was not significant (p=0.693). In addition, the mean number of diagnostic tests showed no statistical difference between the two groups. The mean cost for diagnostic tests within each method was not affected from demographic and socialeconomic factors. The mean drug costs were 152 Euros for LC method and 416.1 Euros for the MC method (p<0.001), (Table 2). For the MC method the average length of stay [LOS] was 11 days and for the LC method only 5 days [mean LOS for LC method 5.06± 6 days vs 10.72± 7.3 days, respectively for the MC method; p<0.001). According to the Greek NHS prices the mean per diem for the so called “hotel services” cost was 38.37 Euros, thus the mean hospital bed day cost in the surgical ward in the MC group was 422 Euros versus 195.7 Euros in the LC group. For patients between 25 and 49 years, the mean length of stay had no statistical significant difference between the two methods. Firstly, it is worth mentioning that patients over 65 years old or with a “Pensioner” status undergoing the LC intervention presented almost 50% higher LOS compared to all other patients. Secondly, Traders and Employees in the Public Sector had the lower LOS.

On the other hand, the relevant indirect cost due to sick-leave was almost double (5 days and 310 Euros for the LC and 11 days and 671 Euros for the MC). Therefore, a 95% confidence interval for the total cost (direct and indirect) for the state or/and the insurance fund was 1.986, 4±246, 9 Euros for the LC method costs and 2.372, 2±610, 5 Euros for the MC.

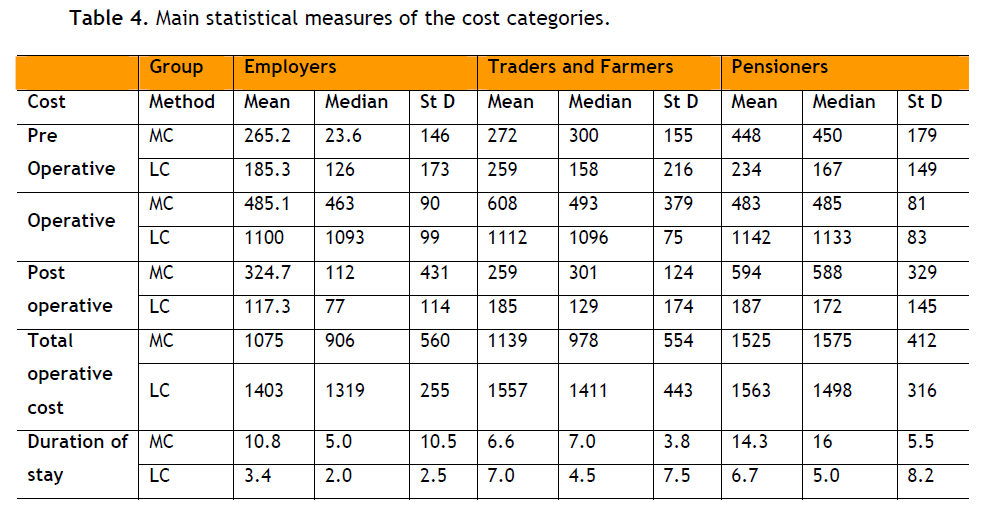

Socio-economic Cluster Analysis

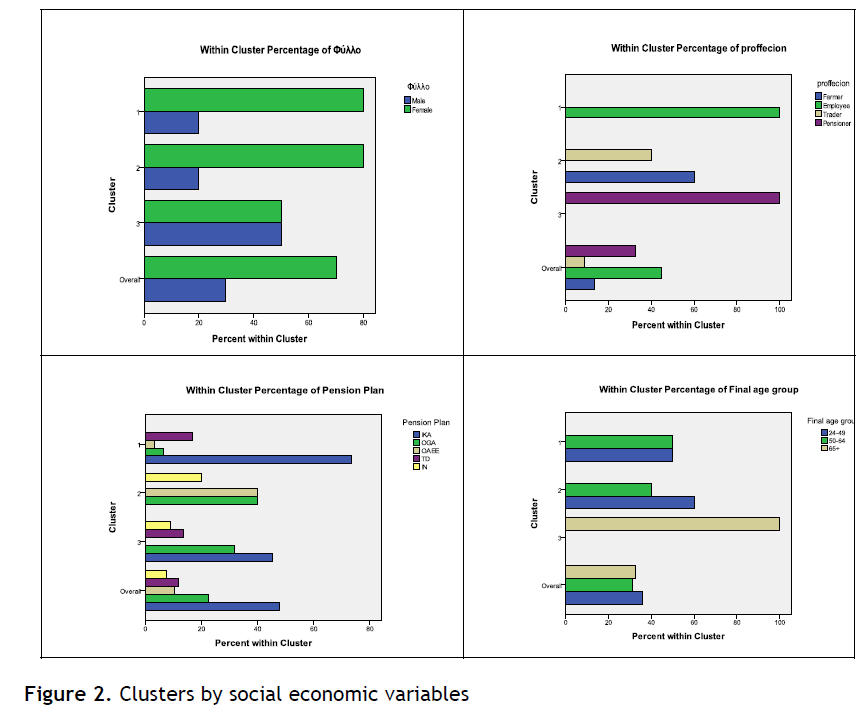

For a further analysis of the data, we use a second division of cost in the three following categories. For the pre-operative cost the mean cost is 247 Euros, with 95% confidence interval between 202 and 292. The standard deviation is 184 Euros and the range of values is 911 Euros (max value 1001 Euros and min value 90 Euros). For the intaoperative cost the mean cost is 964 Euros, with 95% confidence interval between 894 and 1034. The standard deviation is 287 Euros and the range of values is 988 Euros (max 1261. min 273). For the postoperative cost the mean cost is 218 Euros with 95% confidence interval between 161 and 276 Euros. The standard deviation is 235 Euros and the range of values is 1195 Euros (max 1225 and min 30). The basics characteristics of the above analysis are the range and the dispersion, which are sufficiently large compared with the mean [Table 4] . More over, data segmentation took place using clustering technique and taking into account cost variables (pre-. intaand post-operative cost), social economics and demographic variables (sex. age. profession and pension plan). Using the demographic variables (Figure 2) the first group can be named Employers, the second Traders and Farmers and the third Pensioners.

Figure 2: Clusters by social economic variables

According to the cost variables statistical significant differences are presented between groups for pre and post operative cost. The differences are statistical significant between employers and pensioners (Kruskal Wallis H test. p-value = 0.14 and 0.10 respectively). Within the groups and taking into account the method of the surgery, statistical significant differences appeared: For the employers operative cost for LC method is 1100 Euros and for MC method 485 Euros (Mann Whitney U test. p-value<0.05). For the farmers and traders small, not statistical significant, differences are appeared for pro, post and operative cost but the difference for the total cost is statistical significant (Mann Whitney U test. p-value=0.04). For the pensioners statistical significant differences are appeared for pro (Mann Whitney U test , p-value=0.009), post (Mann Whitney U test, p-value=0.001) and operative cost (Mann Whitney U test, p-value<0.05).

Regression Analysis

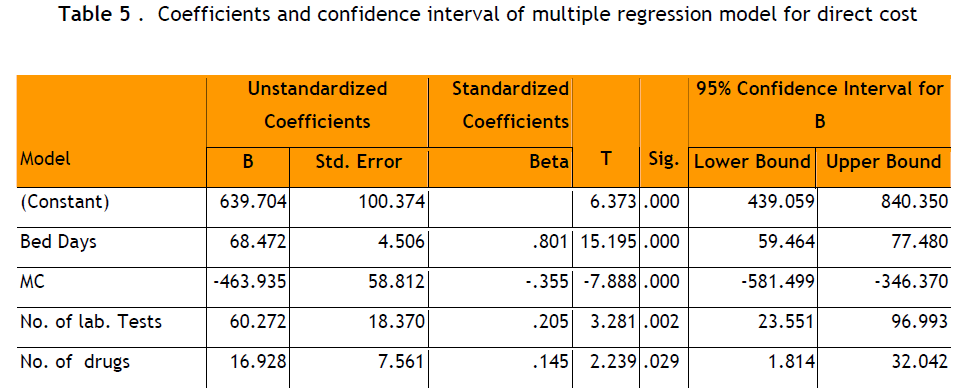

Finally, multiple regression analysis was performed by the stepwise regression method to determine any other importance of factors associated with mainly direct cost. Surgery method, length of stay, number of diagnostic tests and number of drugs were selected as significant factors associated with total mean cost. The unstandardized correlation coefficients were presented in Table 5. Regression analysis showed that these factors were significantly associated with total cost (R2 =0.89. p<0.001).

Concerning further regression analysis, we assume that the 3 different cost components act as dependent variables, while sex, age, profession, method of operation etc. act as independent variable. Adjusted R square was poor both in pre-operative cost (0.172) and post operative cost (0.3). On the contrary adjusted R square was quite strong (0.8) in operative cost, mainly and obviously related to the method of operation. Regression analysis of ALS versus other sample characteristics gave similarly low adjusted R square (0.191).

Discussion

Today where significant economic constraints, coupled with continuously escalating medical costs, and limited health care resources such as personnel time, facilities and equipment, analysis on costs of various interventions become essential not only for medical practitioners and hospital administrators, but also for governments and health-care policymakers.

Cholecystectomy, which can be performed with either laparoscopic or open surgery, remains the definitive treatment for a symptomatic gallstone disease [6] . According to Keus F and his colleagues [14,15] who conducted a review of all published randomised trials in patients with symptomatic cholecystolithiasis comparing any kind of minimal incision cholecystectomy to any kind of open cholecystectomy, laparoscopic seem to be equivalent in mortality, complications and recovery. Considering the results of this review we aimed to conduct a cost minimization approach.

The present study evaluates the total [direct and indirect] cost of two surgical procedures (laparoscopic cholecystectomy versus open surgery). According to the results, the total cost was quite similar between patients in the two groups. Similarly, no significant difference appeared in mean direct hospital cost after LC and MC surgery. When the two interventions are compared concerning the “25-65” group of age, the MC method was cheaper than the LC one. On the contrary, the mean intra operative cost was significantly lower in LC group versus MC group. These findings are in line with a report [16] which indicated that operative costs would be lower in case more than 70 cholecystectomies were performed with the laparoscopic approach annually rather than with the open technique, using disposables materials. At our hospital more than 200 cholecystectomies are performed with the laparoscopic technique annually.

Further to our study, a recent review conducted by Nilsson and his colleagues [11] concluded that total costs did not differ between mini-laparotomy cholecystectomy and laparoscopic cholecystectomy with highvolume surgery and disposable trocars, whereas laparoscopic cholecystectomy was more expensive with fewer operations and disposable trocars. A cost-minimization analysis16 concluded that laparoscopic cholecystectomy was a cost-saving surgical strategy compared to conventional open cholecystectomy if at least 68 patients were operated on annually.

Hospital stay was significantly lower in patients underwent LC surgery as well as operative time within the theatre. These findings are similar with previous reports in the literature [11-12,14-15] . In a study, Kesteloot K and his colleagues17 suggested that the costs and effects of open versus laparoscopic cholecystectomies are comparable, from the point of view of hospitals and patients. From a financial viewpoint, hospitals have to weigh the higher costs of the laparoscopic equipment against the lower variable costs due to the shorter postoperative length of stay.

According to the present study, the average sick-leave for patients after LC operation and treatment is half compared to those followed an MC operation and treatment. Consequently, the relevant indirect cost is lower for the LC rather than for the MC method.

Finally, Srivastava and his collegues [18] performed a cost-effectiveness analysis to evaluate the total cost of minilaparotomy cholecystectomy and laparoscopic cholecystectomy. One hundred adult subjects with painful gallstone disease were randomized while the total cost of each case included diagnostic tests cost, cost of disposable articles for operation, cost of drugs cost of hospital stay and cost of operation including anaesthesia. Minilaparotomy and laparoscopic cholocystectomies were done with reusable instruments. The authors concluded that laparoscopic technique is a more costeffective method from a societal viewpoint for treatment of gallstone disease. These findings compare well with our study if we consider the lower indirect cost of LC due to earlier return to work.

On the contrary Calvert and his colleagues [8] evaluated in hospital costs for laparoscopic and small-incision cholecystectomy using results of a single blind prospective randomised trial and showed that small-incision cholecystectomy was 29% less expensive than the laparoscopic procedure. Costs of equipment and disposables themselves accounted for most of the difference. Results also suggested that costs to patients and society from time lost away from work may be lower for minicholecystectomy. However, we have to consider that the economic success of the LC method depends on appropriate patient selection and well trained staff [13] . In summary, two early reports [16,18] found that laparoscopic cholecystectomy is less costly than minilaparotomy cholecystectomy, whereas one study found that laparoscopic cholecystectomy was more expensive than minilaparotomy cholecystectomy [8] . It can be concluded that, once sufficient experience with laparoscopy can achieve, most hospitals could realise cost savings by switching as much as medically justified, to laparoscopic procedures. In Greece, the laparoscopic approach offers a decrease in sick-leave and intra-operative cost and therefore, may influence third-party payers and institutional administrators in the name of cost constraints.

In order to interpret our data properly, the limitations of our study must be addressed. One limitation of the study is the number of patients enrolled compared to other studies. Moreover, risk factors that may affect postoperative clinical outcomes were not evaluated. However, our study showed that the laparoscopic method is a cost saving approach, concerning the utilization of health care resources and rate of earlier return to work, which consequently calculates lower indirect cost. Whether the discrepant economic results of studies represent issues related to volume or other factors remains unknown. More studies with standard definition of hospital cost components and economic methodologies are required to delineate the true economic effect of LC method and its impact on selected patients.

3477

References

- Konstadoulakis MM, Antonakis PT, Karatzikos G. Alexakis N. Leandros E. Intraoperative Findings and Postoperative Complications in Laparoscopic Cholecystectomy: The Greek Experience with 5.539 Patients in a Single Center. Journal of Laparoendoscopic & Advanced Surgical Techniques 2004; 14(1): 31-36.

- J?rgensen T. Treatment of Gallstone Patients. Copenhagen: National Institute of Public Health. Denmark and Danish Institute for Health Technology Assessment, 2000.

- Gurusamy KS., Samraj K. Early versus delayed laparoscopic cholecystectomy for acute cholecystitis. Cochrane Database Syst Rev 2006; 4:CD005440.

- Kalser SK. National Institute of Health Consensus Development Conference Statement on Gallstones and Laparoscopic Cholecystecomy. Am J Surg 1993;165(1): 390?398.

- Keus F., Gooszen HG., Van Laarhoven CJ. Systematic review: open. s mall-incision or laparoscopic cholecystectomy for symptomatic cholecystolithiasis. Aliment Pharmacol Ther 2009; 29 (4):359-78.

- J?nsson B., Zethraeus N. Costs and benefits of laparoscopic surgery--a review of the literature Eur J Surg Suppl 2000; Suppl.585:48-56

- Barkun JS., Caro JJ., Barkun AN., Trindade E. Cost-effectiveness of laparoscopic and mini-cholecystectomy in a prospective randomized trial. Surg Endosc 1995; 9(11): 1221?1224.

- Calvert NW., Troy GP., Johnson AG. Laparoscopic cholecystectomy: a good buy? A cost comparison with smallincision (mini) cholecystectomy. Eur J Surg 2000; 166(10): 782–786.

- McGinn FP., Miles AJ., Uglow M., Ozmen M., Terzi C., Humby M. Randomized trial of laparoscopic cholecystectomy and mini-cholecystectomy. Br J Surg 1995; 82(10): 1374?1377.

- McMahon AJ., Russell IT. Baxter JN. Ross S. Anderson JR. Morran CG. Sunderland G. Galloway D. Ramsay G. O΄Dwyer PJ. Laparoscopic versus minilaparotomy cholecystectomy: a randomised trial. Lancet 1994; 343(8890): 135–138.

- Nilson E., Ros A., Rahmqvist M., Backman K., Carlsson P. Cholecystectomy: costs and health-related quality of life: a comparison of two techniques. International Journal for Quality in Health Care 2004; 16(6): 473?482.

- Polyzos N., Economou Ch., Zilidis Ch. National Health Policy in Greece: Regulations or Reforms? The Sisyphus Myth European Research Studies 2008; XI (3): 91-118.

- Tragakes E., Polyzos N. Evolution of health care reforms in Greece: charting a course of change. International Journal of Health Planning and Management 1998; 13(2): 107-130.

- Keus F., de Jong JAF., Gooszen HG., van Laarhoven CJHM. Laparoscopic versus small-incision cholecystectomy for patients with symptomatic cholecystolithiasis. Cochrane Database of Syst Rev 2006; 4: CD006229.

- Keus F., de Jong JA., Gooszen HG., van Laarhoven CJ. Small-incision versus open cholecystectomy for patients with symptomatic cholecystolithiasis. Cochrane Database Syst Rev 2006; 18(4):CD004788.

- Berggren U., Zethraeus N., Arvidsson D., Haglund U., Jonsson B. A costminimization analysis of laparoscopic cholecystectomy versus open cholecystectomy. Am J Surg 1996; 172(4): 305?310.

- Kesteloot K., Penninckx F. The costs and effects of open versus laparoscopic cholecystectomies Health Econ 1993; 2(4):303-12.

- Srivastava A., Srinivas G., Misra MC., Pandav CS., Seenu V. Cost-effectiveness analysis of laparoscopic versus minilaparotomy cholecystectomy for gallstone disease, A randomized trial. Int J Technol Assess Health Care 2001; 17(4):497-502.